Blog

DeMarco Dissects Arguments for Principal Forgiveness

In prepared remarks for a speech to be delivered to the Brookings Institute today the Federal Housing Finance Agency’s (FHFA) acting director laid out in detail the reasons for the agency’s resistance to the concept of principal reduction of Fannie Mae and Freddie Mac (ENTERPRISE) loans. Edward J. DeMarco has been under increasing pressure to implement such a program, already in place for many servicers participating in the Home Affordable Modification Program (HAMP).</p

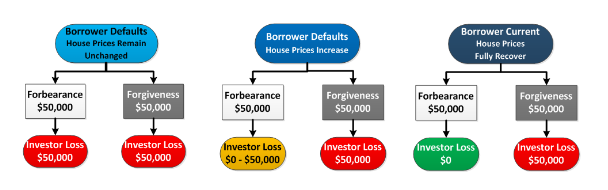

Principal forbearance means setting aside the required amount of the principal. The homeowner does not make payments on that portion of the principal nor is he charged interest on the amount. This approach allows the Enterprises to reduce borrowers’ monthly payments while avoiding principal write-offs. </p

Principal forbearance operates in a manner very similar to shared appreciation except that with forbearance the investor’s share of any appreciation is paid first and is capped at the time of loan modification to the amount of principal forborne. If prices rise above that amount the borrower captures all of the appreciation. There is also no need for infrastructure changes to account for future assets and liabilities as in shared appreciation.</p

Under HAMP, an affordable payment is achieved by taking specified sequential steps (or a waterfall). First the arrearages including accrued interest and escrow advances are capitalized. Next the interest rate is reduced in increments of 1/8th to get as close as possible to 31 percent of the homeowners gross monthly income without going below 2 percent. If the payment has not reached 31 percent after these steps then the term of the loan is extended for up to 480 months and the loan re-amortized. If the payment is still outside program parameters then the servicer may provide principal forbearance down to the larger of 100 percent of the property’s current market value or 30 percent of the unpaid principal balance.</p

Where an Enterprise loan has not qualified for HAMP the Enterprises have employed a proprietary model which also features a waterfall for loans above 115 percent loan-to-value (LTV) ratio but forbearance becomes the second step in the process and the interest rate is set to a fixed rate, currently 4.625 percent. These changes must result in at least a 10 percent reduction in the homeowners’ principal and interest payments.</p

The Treasury Department has acknowledged the benefit of this approach and recently announced a Tier 2 HAMP program that mirrors this proprietary modification program.</p

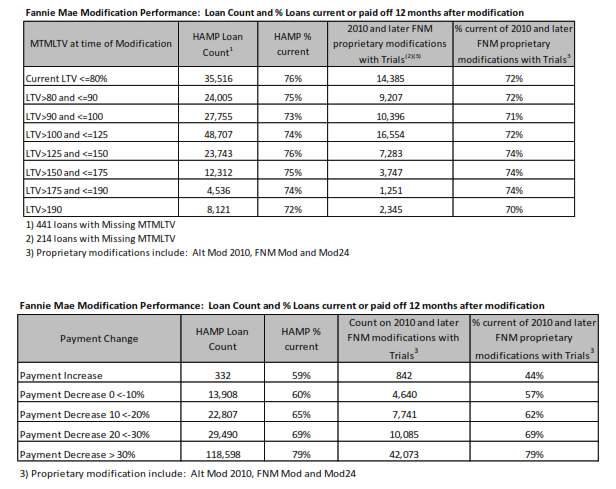

DeMarco said there are many issues involved in the decision on whether the Enterprises should employ principal reduction but data on modifications on its loans show that performance is not strongly related to current LTV but is a function of the payment change. More complex analysis of other studies show some effect of LTV but not as strong as that of payment reductions</p

In the original HAMP, principal forgiveness has always been permitted but was rarely used. In 2010 to encourage greater use in loans with LTVs over 115 percent Treasury added the HAMP Principal Reduction Alternative or PRA. This is an investor not a borrower option and HAMP does not require the lender to offer it even if the servicer determines it has a Net Present Value (NPV) superior to a standard HAMP modification. Still few investors chose to use the program so earlier this year Treasury announced its intention to triple its current payment incentive to investors who use PRA.</p

Both original HAMP and HAMP PRA focus on the borrower’s ability to pay but PRA also addresses the willingness to pay on the theory that an underwater borrower may not continue to be willing to make mortgage payments even if those payments are lower. By forgiving a portion of that balance the lower LTV should, it is thought, improve that willingness. </p

In fact, historical data has shown that the probability of default correlates with the LTV ratio – the higher the ratio the greater the likelihood of default. So, in theory, by forgiving principal and reducing a borrower’s current LTV ratio the probability of default and losses are both reduced. This relationship between default and LTV is supported by previous analytic work and embedded in the HAMP NPV model and thus explicitly factored into the FHFAs repeated analysis of principal forgiveness.</p

Some proponents of forgiveness would limit eligibility in various ways such as prohibiting it in cash-out refinance loans or loans with mortgage insurance but there is no consensus on what such limits should be. If the Enterprises were to apply forgiveness it would have to be clear and transparent, have a basis in the conservatorship mandate, and would have to be clearly and publicly described so that more than a thousand mortgage servicers could apply the rules the same way.</p

At the most basic level, the comparison between principal forgiveness and principal forbearance is related to who gets the upside. For both, if a borrower defaults, the Enterprises lose the same amount. However, if a borrower performs successfully on the modification, in forbearance the Enterprises retain an upside to the forborne amount but in forgiveness the borrower retains the upside.</p

</p

</p

The basic relationship between forbearance and forgiveness largely explains the rationale he presented to Congress in January, DeMarco said. But any analysis of employing forgiveness also requires that FHFA look beyond the NPV results to the operational costs of implementing the program and the impact of borrower incentive effects given that three quarters of the Enterprise’s deeply underwater borrowers are current.</p

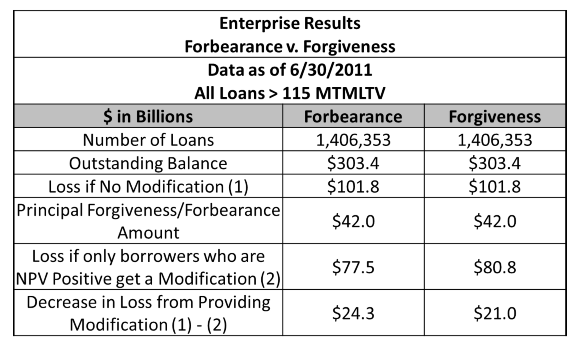

FHFA has gone beyond that January analysis. The later analysis assumed that all ENTERPRISE loans with LTVs greater than 115 percent as of June 20, 2011, whether current or not would be modified. The analysis looked at two modifications for each loan; one with principal forgiven down to 115 percent, in the other the principal was forgiven. </p

</p

</p

The analysis showed that:</p<ul

Borrowers receiving forgiveness default less often however losses associated with the forgiveness write-offs more than offset the savings from the lower re-default rates as the present value of the cash flows to an investor is higher for forbearance than forgiveness as the upside return of the forborne amount is preserved.</p

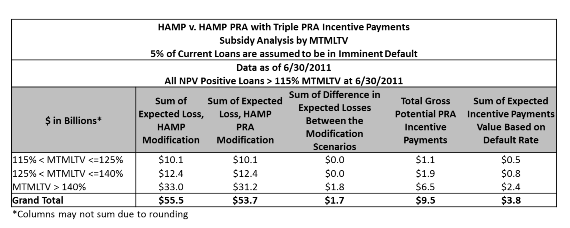

FHFA is still analyzing whether the Enterprises will offer principal forgiveness as part of HAMP with the triple incentives provided by Treasury. However, DeMarco said he was presenting preliminary findings from incorporating those incentives into models and including changes bases on critiques of the earlier analysis. For example, the earlier analysis used FICO and debt-to-income ratios from the time of loan origination which probably overstated the credit quality of the loans in the current economy. An adjustment was made to those numbers and the new analysis used more granular estimates of home value as well.</p

In addition, the new estimate eliminates borrowers who are current on their mortgages along with a factor to account for current loans that might default. Table 7 shows that Enterprise losses on these loans are expected to be $63.7 billion if they are not modified. Losses would be 55.5 billion with forbearance and 53.7 billion with forgiveness. Because the Enterprises would receive the tripled incentive payments for principal forgiveness, PRA reduces the Enterprise losses by $1.7 billion.</p

</p

</p

The total PRA incentive payments are $9.5 billion and the expected PRA payments considering future defaults are $4.8 billion On an NPV basis this analysis would show a positive benefit to the Enterprises of $1.7 billion and Treasury incentive payments of $3.8 billion for a net cost to the taxpayer of $2.1 billion.</p

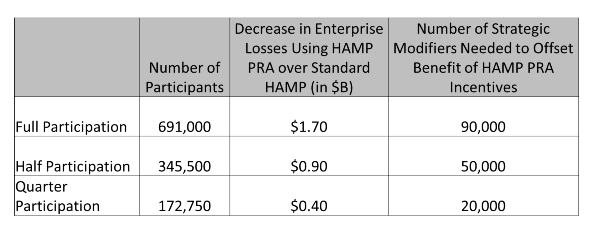

Another factor that needs to be considered is borrower incentive effects. How many borrowers who are current on their loans will be encouraged to either claim hardship or go delinquent to obtain principal forgiveness? This is a particular concern for the Enterprises because they cannot pick and choose where forgiveness makes sense, they must develop a program that can be implemented by one thousand servicers and sellers. The Enterprises would also have to publicly announce the availability of the program </p

FHFA has no idea how many current borrowers would seek to become strategic modifiers but, through a complex set of parameters reducing the population of eligible borrowers to probable borrowers FHFA came up with the number of strategic modifiers required to completely offset the benefit of HAMP PRA incentives to the Enterprises.</p

</p

</p

Finally there are the operational costs of implementing principal reduction including the impact on multiple technologies in the loss mitigation and loan accounting infrastructure. DeMarco said FHFA is still evaluating the costs, but they are not trivial. There would also be indirect costs such as developing guidance and training for servicers, and opportunity costs of diverting existing resources from other programs.</p

DeMarco said that FHFA would make its decision on whether the Enterprises should offer principal forgiveness with the triple incentives based on the issues he described. But whether Fannie Mae and Freddie Mac forgive principal or not, the universe of Enterprise borrowers who are potentially eligible is well less than one million households, a fraction of the estimated 11 million underwater borrowers in the country today. “This is not about some huge difference-making program that will rescue the housing market. It is a debate about which tools, at the margin, better balance two goals; maximizing assistance to several hundred thousand homeowners while minimizing further costs to all other homeowners and taxpayers.”</p

Encouraging the continued success of the larger group of underwater borrowers who have remained faithful to paying their mortgages, DeMarco said, could have a greater impact on the ultimate recovery of housing markets and cost to the taxpayers than the debate over which modification approach offered to troubled borrowers is preferable.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment