Blog

A Different Perspective on Obama’s Bank Fee: An Indirect Attack on Inflation

Yesterday the President announced his intention to propose a Financial Crisis Responsibility Fee that would require the largest and most highly levered Wall Street firms to pay back taxpayers for the extraordinary assistance provided so that the TARP program does not add to the deficit. The fee the President is proposing would:

- Require the Financial Sector to Pay Back For the Extraordinary Benefits Received

- Responsibility Fee Would Remain in Place for 10 Years or Longer if Necessary to Fully Pay Back TARP

- Raise Up to $117 Billion to Repay Projected Cost of TARP:

- President Obama is Fulfilling His Commitment to Provide a Plan for Taxpayer Repayment Three Years Earlier Than Required

- Apply to the Largest and Most Highly Levered Firms

The immediate reaction from market watchers: THIS WILL INHIBIT BANK LENDING AND FURTHER SLOW THE RECOVERY PROCESS. One source actually says this will slow bank lending by $1 TRILLION.

I don't agree with that stance. Before going deeper into my perspective, below is some background on the money creation process. Skip if you already have a firm understanding.

————————————————————————————-

The goal of a bank is to maximize net worth for its shareholders. This objective is achieved by lending out money at a rate which exceeds the cost of borrowing. Because lending is a risky business (haha do I need to explain that?), shareholders require that banks keep excess reserves to protect the security of their deposits. These reserves are stored in their vaults and are used to meet the demands of depositors.

Banks have three types of assets:

- Liquid Assets like US Treasury bills

- Investment Securities like US Treasury bonds and Agency MBS

- Loans made to corporations and consumers.

The Federal Reserve's role in this whole process is to provide banking services to commercial banks like JP Morgan Chase, Citi, and Bank of America. The Federal Reserve controls the amount of money banks can lend and therefore controls the amount of money in circulation.

There are three ways the Fed does so… they can do this via adjustments to the required reserve ratios, raising or lowering the discount rate, and by purchasing or selling assets to/from banks via open market operations (purchasing TSYs and MBS from banks).

Required reserve ratio is the minimum percentage of deposits that banks must hold as reserves. When banks have extra reserves, they are able to lend out those funds, which creates money.

The discount rate is the rate at which the Fed will lend reserves to banks in need. Currently the discount rate is at historic lows which implies banks can borrow cheap excess reserves to make new loans (thus creating money and earning more profit).

Open market operations are the purchase or sale of govern securities. The Fed has taken additional actions to provide liquidity in the marketplace by purchasing agency MBS in the open market. When the Fed buys from banks, they are taking assets of their balance sheet in exchange for money (reserves). The more the Fed buys in the open market, the more excess reserves banks will accumulate and therefore create money by lending to businesses and households.

Whenever the banking system has excess reserves, banks can create new money. Whenever the banking system lacks reserves, they decrease their loans and rebuild reserves…this slowly the growth rate of money.

—————————————————————————————–

I have a bone to pick with the folks who say this will slow down bank lending. I have an even bigger bone to pick with the folks who say this will slow down bank lending AND have been shouting BENrnIS PRINTING MONEY!!!! INFLATION INFLATION INFLATION!!!

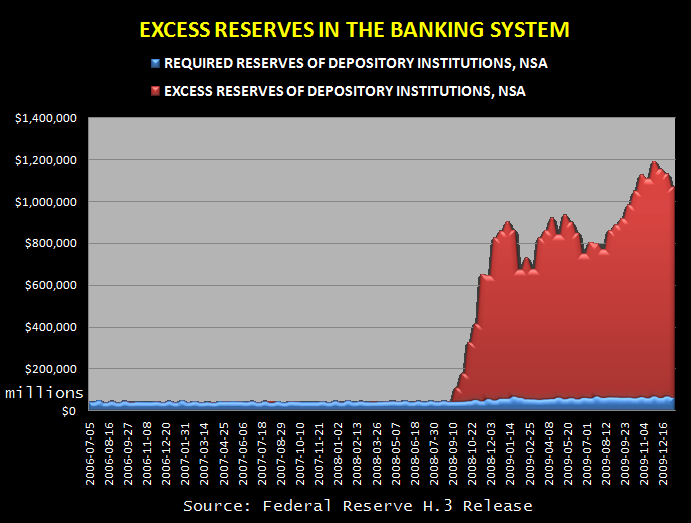

In July, 2009, the New York Federal Reserve released a research paper titled WHY ARE BANKS HOLDING SO MANY EXCESS RESERVES?

Here is an excerpt:

“Since September 2008, the quantity of reserves in the U.S. banking system has grown dramatically,rnas shown in Figure 1.1 Prior to the onset of the financial crisis,rnrequired reserves were about $40 billion and excess reserves werernroughly $1.5 billion. Excess reserves spiked to around $9 billion inrnAugust 2007, but then quickly returned to pre-crisis levels andrnremained there until the middle of September 2008. Following therncollapse of Lehman Brothers, however, total reserves began to growrnrapidly, climbing above $900 billion by January 2009. As the figurernshows, almost all of the increase was in excess reserves. Whilernrequired reserves rose from $44 billion to $60 billion over thisrnperiod, this change was dwarfed by the large and unprecedented rise inrnexcess reserves.“

Below is a chart from the Federal Reserve's H.3 Data

The spike in excess reserves in the banking system is obvious.

These excess reserves have yet to be lent by banks to consumers and small businesses…regardless of President Obama's numerous requests. (This is a topic forrnanother conversation…but there isn't exactly a surplus of qualifiedrnborrowers out there either).

While I acknowledge the anxieties of those who state thern”responsibility fee” will further slow already stagnate lendingrnmarkets, I think we should take a step back and look at this fromrnanother perspective.

According to the “Financial Crisis Responsibility Fee” fact sheet…

“The fee the President is proposing would be levied on the debts of financial firms with more than $50 billion in consolidated assets, providing a deterrent against excessive leverage for the largest financial firms. By levying a fee on the liabilities of the largest firms – excluding FDIC-assessed deposits and insurance policy reserves, as appropriate – the Financial Crisis Responsibility Fee will place its heaviest burden on the largest firms that have taken on the most debt. Over sixty percent of revenues will most likely be paid by the 10 largest financial institutions.”

These are the large commercial banks who have the most reserves to lend, the banks who are “too big to fail”. If these reserves were turned into money via making loans to consumers and small business, it would most definitely inflate the money supply. THIS IS WHERE INFLATIONARY FEARS ARE ROOTED.

With that in mind, given the current sensitive state of the long end of the yield (nervous about rate hikes and inflation), perhaps the Obama Administration is indirectly raising the Fed Funds rate for the banks who pose the biggest inflationary threat to the economy?

Instead of using a traditional Federal Reserve policy tools, all three of which are described above, perhaps the Fed and President Obama are imposing this bank tax as a means of draining excess reserves in the banking system? Perhaps this is just a way to start fighting inflation before it becomes a bigger problem?

For those of you who are nervous about a continued slowdown in bank lending, there will still be a ton of excess reserves left in the banking system to lend out. You should also read the New York Federal Reserve paper I called attention to above.

Unfortunately, when you strip out all the political positioning that is behind this “fee”, the crux of the bank lending problem is no where near in “recovery mode”. We still have a major credit crisis going on here…the credit of all the prospective borrowers in this country has been slowly deteriorating over the past two year. Banks have no incentive to lend excess funds to borderline borrowers.

Until the credit of credit of prospective borrowers is repaired, which will require job creation, the macroeconomic recovery (especially housing) will be a SLOW STAGNATE PROCESS.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment