Blog

CBO Evaluates Potential Costs of a Large-Scale Refinancing Program

Thernnon-partisan Congressional Budget Office (CBO) just released a working paperrnentitled An Evaluation of Large-Scale MortgagernRefinancing Programs in which it analyzed a large-scale program that wouldrnrelax current income and loan-to-value restrictions for borrowers who wish tornrefinance mortgages currently held by Fannie Mae, Freddie Mac, or the FederalrnHousing Administration. The analysis uses an estimate of the increasedrnrefinancing that would occur and how future default and prepayment behaviorrnwould be affected by such refinancing. </p

The paper was written by Mitchell Remy andrnDamien Moore, both of the Financial Analysis Division of the CBO and DeborahrnLucas, Sloan School of Management at the Massachusetts Institute of Technology.</p

Despiternthe gradually recovering economy, the paper says, the housing market remainsrnweak and, in addition to the large number of mortgage delinquencies andrndefaults many homeowners are unable to refinance and take advantage of recordrnlow interest rates. This has prompted arnnumber of proposals for federal programs to provide opportunities for refinancingrnwhich would free up household income for non-housing expenditures as well asrnhelp some homeowners avoid future default.</p

Thernlack of refinancing is driven by weakened household balance sheets that make itrndifficult for some borrowers to meet debt-to-income (DTI) ratios; otherrnhomeowners find their equity eroded by falling house prices and cannot qualifyrnfor refinancing based on the loan-to-value (LTV) ratios of their homes. The increased stringency of underwritingrnrequirements on the part of the government sponsored enterprises (GSEs) and FHArnhave also contributed to the inability of others to qualify for refinancing. </p

Therngovernment has launched several efforts to assist such homeowners but programrnfeatures and eligibility criteria have excluded a significant number ofrnhomeowners who might have benefited. rnThese efforts have also been restricted to homeowners with mortgagesrninsured by the GSEs or other Federal programs representing 56 percent of allrnoutstanding loans.</p

But,rnwhile mass refinancing of these loans might save the government some eventualrnlosses because of future defaults, mortgage investors would experience losses</bthrough loans that are prepaid more quickly than without such programs. Many of these losses would hit taxpayersrnthrough mortgage-backed securities held by the Federal Reserve, the GSEs andrnthe Treasury. The stylized refinancing programrnstudied by the authors would increase the availability of refinancing andrnslightly lower its cost. </p

Homeownersrnare generally free to refinance at will, weighing positive factors such as arnlower rate or better terms against the financial costs of refinancing such asrnappraisal costs, settlement fees, and the time and effort involved in thernprocess. That freedom, however, comes atrna cost as investors evaluate prepayment risk and factor that into the price ofrntheir loans.</p

Overrnthe years refinancing has periodically affected large percentages of thernoutstanding mortgage debt, particularly in periods of declining rates and severalrnchanges in the market such as automated underwriting and property-valuationrnmodels, the widespread use of credit scores, auto have increased the likelihoodrnhomeowners will refinance. </p

However,rnunlike similar periods of declining rates, the fact that rates have droppedrnmore than 1.5 percentage points since 2007 has not sparked a refinancingrnwave. This is largely due to thernfinancial crisis. First, a significantrnnumber of mortgages were actually originated during this period ofrnextraordinarily low rates and earlier transactions have more or less drainedrnthe refinancing pool. Then there are thernwidely acknowledged impediments to refinancing the remaining high interestrnloans – home price declines, reduced income or unemployment, continued highrnlevels of consumer debt, and significantly higher underwriting standards. Many loan products such as interest only, norndocumentation, and negatively amortizing loans have been curtailed or haverndisappeared.</p

Thesernimpediments to refinancing are reflected in the unusually high premium overrnface value that investors are willing to pay for MBS with high couponrnrates. The possibility of prepaymentrnusually prevents MBS from rising in price much above par value but the currentrnpricing indicates that investors expect these impediments to last and thusrntheir investment to continue considerably longer than usual. In January of 2011, weekly pricing forrnpremium ($100 par) Fannie Mae 30-year FRM ranged from just below $105 tornconsiderably over $107. The authors sayrnthat, while many factors influence MBS pricing “a strong case can be made forrnlower prepayment expectations as an important component in the price premiumrninvestors are currently willing to pay for those securities.”</p

Thernauthors examined the parameters and criteria of existing refinancing programs</bsuch as the GSE's Home Affordable Refinance Program (HARP) and some programsrnproposed under pending legislation before laying out their designrnconsiderations for a stylized large-scale program. These include whether to include only GSErnguaranteed mortgages or those guaranteed by FHA and private-label mortgages asrnwell. Should only borrowers who arerncurrent on their existing loans be allowed to participate, only those who arerndelinquent, or both? Should guaranteernfees be increased to reduce the federal cost of the program even if it reducedrnthe potential pool of borrowers or should the fees be reduced to generate thernopposite effect? The degree to whichrnunderwriting procedures are waived or fees are waived or subsidized couldrnsignificantly affect participating rates but could result in loans that arernless appealing to investors and thus increase the interest rate on thernloans. </p

Arnfinal consideration, they said, is the degree to which the LTV isrnutilized. Limiting the level of negativernequity may mitigate the severity of the loss in the case of default, a riskrnthat the guarantor already carries and hopes to reduce through granting a lowerrnmonthly cost. Another question isrnwhether a current LTV is required. Waivingrnan appraisal would save the borrower a fee but would deny investors anrnup-to-date assessment of the potential risk of default inherent in the loan.</p

Thernstylized program that emerged from these considerations had the followingrncharacteristics:</p<ul class="unIndentedList"<liItrnwould start in the first quarter of 2012 and be available for one year.</li<liEligiblernloans would be existing mortgages guaranteed by the GSEs or FHA.</li<liThernborrow must be current and never more than 30 days late on the existingrnmortgage during the prior year but there are no limits on the borrowers currentrnincome or on the LTV of the new loan.</li<liThernGSEs and FHA will assess a guarantee fee equal to that charged initially on thernexisting loan. This will be incorporatedrninto the interest rate by the GSEs and charged as an annual premium by FHA.</li<liThernloan will have a fixed rate of interest at the prevailing rate and a 30 year term.</li<liLendersrnand third party fees will be the lesser of 1 percent or $1000 to process thernloan.</li</ul

Thernauthors estimate that the potential target audience for the program isrnborrowers with mortgages in existing MBS with outstanding balances of $4.3rntrillion as of June 1. Of that total,rnthe GSEs guarantee $3.5 trillion. Thesernare all fixed rate mortgages. Althoughrnborrowers with adjustable rate mortgages (ARM) would also benefit from thernprogram they, as well as non-traditional and delinquent borrowers were excludedrnfrom the analysis to eliminate certain complexities in estimating incentives.</p

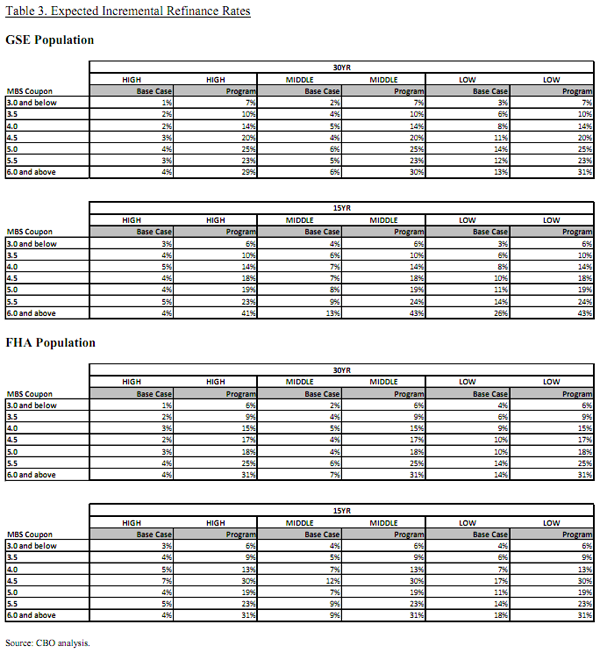

Borrowersrnwere classified by the interest rate on their current mortgage, the term, and riskrncharacteristics that affect their propensity to default on their mortgages. The groups were further characterized by thernborrower FICO score, the mark-to-market LTV on their existing mortgage and itsrnorigination year and the imputed interest rate on a new mortgage. This resulted in classification into 108rndistinct groups representing the combination of two maturities, nine couponrnrate pools, and three risk categories. rnTotal program costs are the sum of the cost per dollar of outstandingrnloans multiplied by the estimated total principal balances across each of thern108 groups.</p

Each group was run through arnmodel to simulate a scenario and determine the incremental refinancingrnattributable to the program and a base case scenario to estimate expected repayments,rndefaults, and loss severities over each group without the program. The analysis then presumed that all borrowersrnhad an LTV of 50 percent, FICO scores of 780, and assumed the new mortgage hadrna rate reflecting market conditions and discounted transaction fees.</p

The difference in prepaymentrnvolumes between the base case and the program model represent the incrementalrnrefinancing attributed to the program over the course of calendar year 2012 andrnthose rates, applied to estimated outstanding principle balances, determine thernexpect dollar volume of the incremental financing.</p

</p

</p

Thernrelaxed underwriting constraints result in identical refinance rates betweenrnhigh, medium and low risk categories with the same MBS coupon in the programrnscenario. Borrowers in the high andrnmiddle risk categories (higher LTV, lower FICO) benefit the most from thernprogram based on the increase in refinance rates between the base case andrnprogram scenarios. Because these groupsrnare a small portion of the borrower population, however, the greatest number ofrnincremental loans is expected in the low risk group where borrowers are likelyrnto be attracted by the lower costs of the program.</p

Arnprogram such as that analyzed offers benefits to homeowners including lower monthlyrnpayments resulting from lower interest payments and lower principal payments becausernof the re-amortization of the loan. Thisrnresults in an increase in disposable income which could help the economy,rnassist the borrower in paying down other debt, and in some cases help prevent eventualrndefault. </p

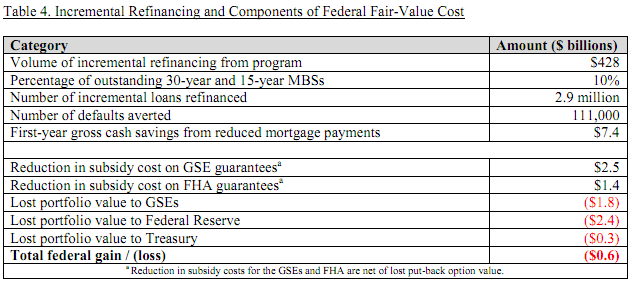

Thernauthors estimate that the program would result in incremental refinancing ofrn2.9 million mortgages with first year gross cash savings from reduced mortgagernpayments of roughly $2,600 per borrower or a total of $7.4 billion.</p

Thernmodel predicts that approximately 111,000 fewer loans will default as a resultrnof this program, in comparison to the approximate 4 million borrowers currentlyrnpast due on their mortgages.</p

Thernresults have cost implications for the GSEs, FHA, the Federal Reserve, and thernTreasury Department. Because of theirrnmix of credit guarantees and portfolio investments the GSEs will experiencernboth gains and losses; FHA will see gains from credit guarantees and the Fedrnand Treasury will face losses through their investments in MBS. Total federal losses from investment will bern4.5 billion resulting in a net federal loss from the program of $0.6 billion.</p

</p

</p

Non-governmentrninvestors hold 65 percent of the outstanding MBS included in the analysis andrnalso held a greater share of older, higher coupon securities than the Federal share. Non-federal investors were expected to sufferrna fair-value loss of $13 to $15 billion, triple the federal loss.</p

Thernauthors see several impediments to program implementation. One is the possible inability orrnunwillingness of lenders to scale up quickly to meet program demand, especiallyrnin light of the low origination volumes in recent years. A second obstacle is the willingness ofrnsubordinate lien holders to make the financial or operational considerationsrnnecessary to facilitate refinancing the first mortgage and private mortgagerninsurers must agree to the terms of the refinancing if insurance will bernneeded. The authors assume that thernpotential of reducing default may be attractive enough to convince these thirdrnparties to participate. If this is notrncorrect the number of participants in the program may be reducedrnsignificantly. Finally, the programrncould be imperiled by rising interest rates during the program and could bernaffected either positively or negatively by the direction of housing pricesrnwhich, if rising, may allow more homeowners to qualify for this or other programsrnand if falling may lessen the numbers who are eligible or drive more borrowersrninto default.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment