Blog

CoreLogic Provides Early Estimate of HMDA Origination Data

Data collected from lenders under thernmandate of the Home Mortgage Disclosure Act (HMDA) is due to be released laterrnthis month but CoreLogic is advancing its own estimate of the headline data,rnthe number and volume of first lien mortgages originated for purchase andrnrefinance in 2014. The company’s ownrnnumbers were released in an article by CoreLogic senior economist Molly Boeselrnon the company’s blog.</p

Passed originally in 1975, HMDArnrequires many financial institutions to maintain, report, and publicly disclose</binformation on such mortgage metrics as mortgage denial rates, borrower andrnapplicant information, and mortgage pricing in addition to origination numbers.rnResponsibility for the data was transferred from the Federal Reserve Board to thernConsumer Financial Protection Bureau in 2011. CFPB's HMDA report containsrninformation used by the mortgage industry, especially mortgage marketrnforecasters, as a benchmark on mortgage originations. In anticipation of thernofficial data there are a number of estimates on the previous year'srnoriginations from varying sources. </p

</p

</p

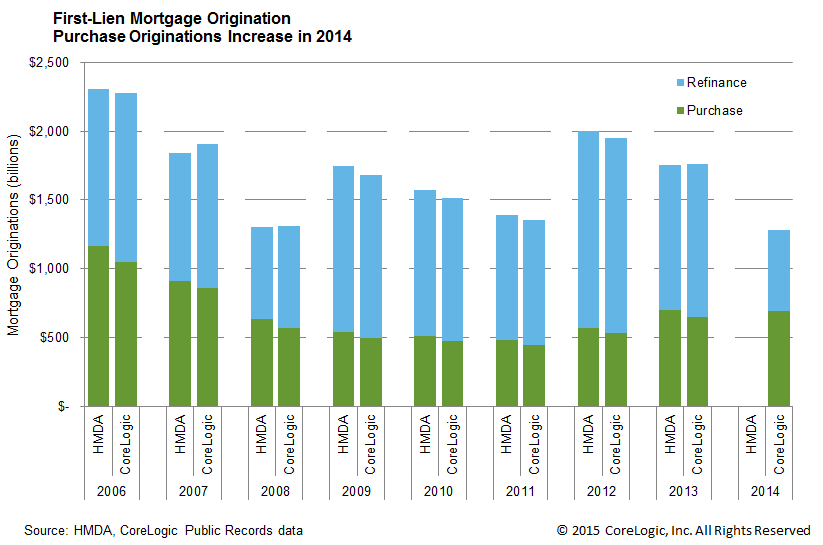

As can be seen from the graph,rnCoreLogic’s estimates regarding purchase money, refinancing, and total dollarrnvolumes have fairly closely tracked the numbers put forth through HMDA. Therncompany said that on average its estimate is within 1 percent of the HMDArnnumbers. This year the company’srnestimates is that the number of mortgage originations in 2014 fell by 30rnpercent from 2013 and the dollar volume was down by 27 percent. CoreLogic projects therefore that HMDA datarnwill peg total originations at a minimum of $1.28 trillion. </p

Not all lenders are required to reportrnHMDA data but most analysts estimate that 95 percent of the mortgage market isrncovered. Taking into account thisrnrelatively small under coverage, CoreLogic puts total originations at aroundrn$1.36 trillion. </p

The drop in originations was attributablernto a decline in refinancing. ThernCoreLogic data puts the decrease in numbers of refinances at 49 percent and inrndollar volume by 47 percent. Purchasernmoney mortgages increased slightly, 5 percent by number and 7 percent by dollarrnvolume, but far from enough to compensate for the refinancing shortfall. CoreLogic put the increase in purchasernoriginations to a 3 percentage point drop in cash purchases and an increase inrnhome value as measured by its own Home Price Index of 7.6 percent.</p

CoreLogic derives its originationrnestimates for public records deed information. From this the company is ablernto determine if there was a mortgage related with a sale and the amount of thernmortgage.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment