Blog

Existing Home Sales Improve from Record Low. "Subpar" Activity Expected

The National Association of Realtors today released Existing Home Sales data for August 2010.</p

HERE is the methodology for data collection</p

Excerpts from the release….</p

SALES</p

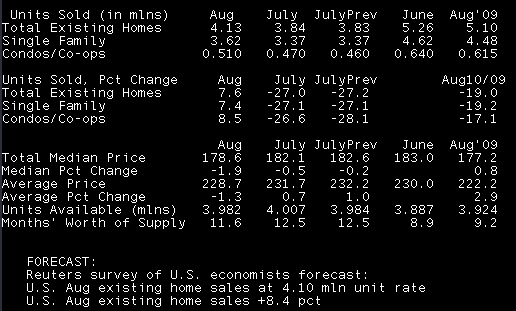

Existing-home sales, which are completed transactions that include single-family, townhomes, condominiums and co-ops, increased 7.6 percent to a seasonally adjusted annual rate of 4.13 million in August from an upwardly revised 3.84 million in July, but remain 19.0 percent below the 5.10 million-unit pace in August 2009.</p

Single-family home sales rose 7.4 percent to a seasonally adjusted annual rate of 3.62 million in August from a level of 3.37 million in July, but are 19.2 percent lower than the 4.48 million level in August 2009.</p

Existing condominium and co-op sales increased 8.5 percent to a seasonally adjusted annual rate of 510,000 in August from 470,000 in July, but are 17.1 percent below the 615,000-unit pace in August 2009.</p

Regionally, existing-home sales in the Northeast rose 7.9 percent to an annual level of 680,000 in August but are 24.4 percent below August 2009. Existing-home sales in the Midwest increased 5.0 percent in August to a pace of 840,000 but are 26.3 percent below a year ago. In the South, existing-home sales rose 5.2 percent to an annual level ofrn 1.62 million in August but are 13.4 percent below August 2009. Existing-home sales in the West jumped 13.8 percent to an annual pace of 990,000 in August but are 16.1 percent lower than August 2009.</p

Distressed homes rose to 34 percent of sales in August from 32 percent in July; they werern 31 percent in August 2009.</p

A parallel NAR practitioner survey shows first-time buyers purchased 31 percent of homes in August, down from 38 percent in July. Investors rosern to a 21 percent market share in August from 19 percent in July; the balance of purchases were by repeat buyers. All-cash sales slipped to 28rn percent in August from 30 percent in July.</p

INVENTORY</p

Total housing inventory at the end of August slipped 0.6 percent to 3.98rn million existing homes available for sale, which represents an 11.6-month supply at the current sales pace, down from a 12.5-month supply in July.</p

PRICES</p

The national median existing-home price for all housing types was $178,600 in August, up 0.8 percent from a year ago. The median existing single-family home price was $179,300 in August, up 1.2 percent from a year ago. The median existing condo price was $174,000 in August, which is 2.8 percent below a year ago.</p

Single-family median existing-home prices were higher in 10 out of 19 metropolitan statistical areas reported in August from a year ago (the price in one of 20 tracked markets was not available). Existing single-family home sales were down in all 20 metro areas from August 2009.</p

The median price in the Northeast was $260,300, up 7.6 percent from a year ago. The median price in the Midwest was $149,600, up 0.4 percent from August 2009. The median price in the South was $155,000, down 1.5 percent from a year ago. The median price in the West was $214,700, which is 2.5 percent below a year ago.</p

Lawrence Yun, NAR chief economist, said home sales still remain subpar. “The housing market is trying to recover on its own power without the home buyer tax credit. Despite very attractive affordability conditions, a housing market recovery will likely be slow and gradual because of lingering economic uncertainty,” Yun said.

Yun added, “Home values have shown stabilizing trends over the past year, even as the economy shed millions of jobs, because of the home buyer tax credit stimulus. Now that the economy is adding some jobs, the housing market needs to steadily improve and eventually stand on its own.”

NAR President Vicki Cox Golder, said consumers have been getting mixed signals about the housing market. “People understand the good affordability conditions with stable home prices in most areas, but they’re concerned about the economy and speculation on Wall Street,” she said. “We need to stick with the facts about the long-term value of homeownership and avoid unrealistic assessments. Tight credit and slow short sales are ongoing problems – expediting short sales will help the market to recover more quickly.”

CHARTS AND MORE COMMENTARY TO BE ADDED

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment