Blog

Expectations for Economy, Housing Subdued in 2nd Half

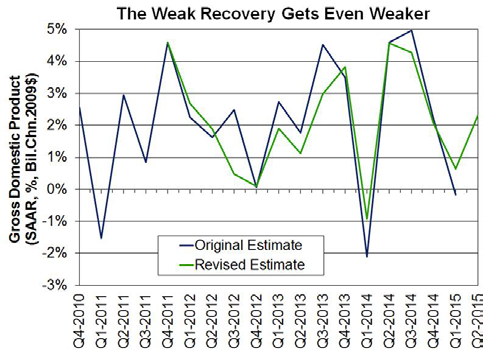

FanniernMae’s economic team said on Monday that the economic outlook for the secondrnhalf of 2015 is less upbeat than anticipated. rnSecond quarter economic growth came in lower than expected and arnbuild-up in business inventories suggest that Fannie Mae’s forecast for thernthird quarter was also too optimistic. rnEven though Q1 growth was improved by later revisions, the full-yearrn2015 growth outlook remains at 2.1 percent. rnDriving that growth will be consumer spending, housing and governmentrnspending.</p

Therndollar will continue to weigh on manufacturing and trade and new declines inrncrude oil prices will create a headwind for the oil and gas sector. Interest rate volatility will probably pickrnup as the September Fed Open Market Committee (FOMC) meeting approaches andrninternational uncertainties, although they have lessened, remain downsidernrisks.</p

</p

</p

FanniernMae’s August forecast notes that it has been nine years since the FederalrnReserve last raised the fed funds rate. rnAfter its last meeting in July the FOMC stated it was looking for “somernfurther improvement” in the labor market before raising the target rate andrnFannie Mae believes that the July jobs report offered sufficient evidence of improvementrnfor the Fed to move. They expect the pace of any hike will be very gradual withrnonly one 25-basis point increase this year. Meanwhile, underlying inflation,rnwhile remaining substantially below the Fed’s target, has firmed from the softrnreadings earlier in the year. In June, the core PCE deflator rose at a 1.6rnpercent annualized rate over the last six months, compared with 0.8 percent atrnthe start of the year. (It should be noted this report was written before thernstock market took its worst plunge in four years on Friday and was continuingrnto decline on Monday.)</p

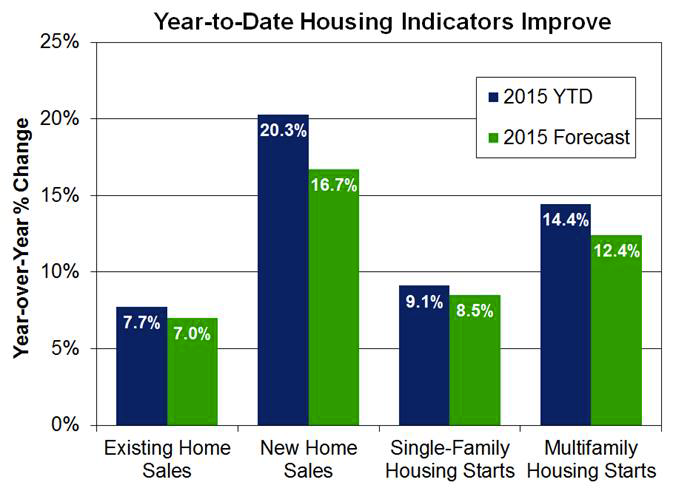

Thernforecast looks to housing to be a bigger contributor to growth this year. Activity was mixed in June but all indicatorsrnwere higher in the first six months of the year than during the comparativernperiod in 2014. Existing home sales in Junernwere at the strongest pace since February 2007 and inventories remain tightrnwhile marketing time is the shortest in four years.</p

</p

</p

Bothrnthe National Association of Realtors (NAR) and CoreLogic said distressed homernsales were at many-year lows. NAR putrnthe June share at 8 percent, the lowest since it began keeping records in late 2008rnwhile CoreLogic showed them accounting for 9.9 percent of total home sales inrnMay, the lowest for that month since 2007.</p

Inrncontrast to the strength in existing home sales, new home sales dropped sharplyrnin June, and sales in the prior three months were revised down significantly whilernleading indicators suggest some weakness for overall sales. The NAR pendingrnhome sales index fell in June for the first time this year. While the purchasernmortgage application index rose during the last week of July, it remains belowrnrecent highs reached in June and early July. The home sales outlook still outshines thatrnof last year as both pending sales and purchase applications are higher than arnyear ago, the latter by 18 percent. </p

Thernsales figures along with lean inventories have supported continued price growth. CoreLogic’s national home price index (notrnseasonally adjusted)-the measure used by the Fed to estimate the value ofrnowner-occupied real estate-rose 1.7 percent in June, its sixth consecutivernmonthly gain and was up 6.5 percent year-over-year, the largest gain since Junern2014. Prices are 7.4 percent below the peakrnreached in April 2006.</p

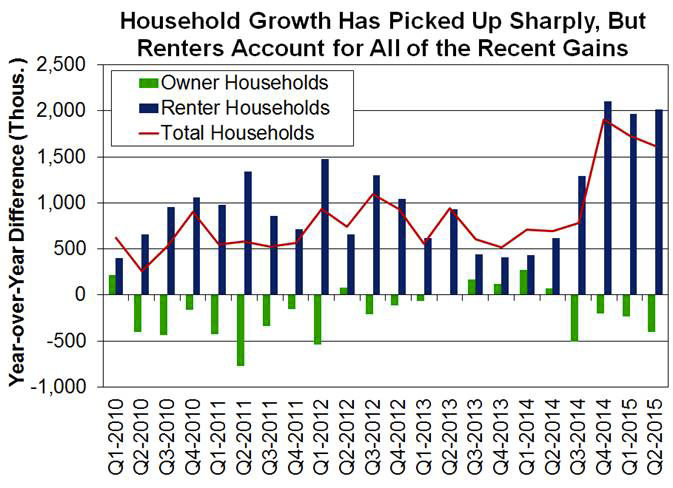

Householdrnformation is finally improving – up by 1.6 million in the second quarterrncompared to a year earlier and the third consecutive quarter of strong annual growth.rnThese new households however, are almost all renting and the rental vacancyrnrate is at 6.8 percent-the lowest rate since 1985. This is putting upwardrnpressure on rents and providing a tailwind to new multifamily construction andrnresidential investment. Meanwhile, the homeownership rate continued to trendrndown, falling 0.3 percentage points in the second quarter to 63.4 percent-thernlowest level since 1967.</p

</p

</p

Fixedrnmortgage rates declined during the last week of July for the third consecutivernweek to 3.91 percent, marking the lowest level since early June. Fannie Mae expects mortgage rates to be largelyrnunchanged for the rest of the year and then are likely to trend up graduallyrnnext year, averaging 4.3 percent during the final quarter of 2016. Gradual easing of credit and low rates shouldrnhelp support housing market recovery even as the Fed begins to hike rates.</p

Therneconomists say that, given stronger data than expected for existing home sales coupledrnwith disappointing data on single-family housing starts they have upgradedrntheir forecast of existing home sales and downgraded projected single-family startsrnand new home sales. Total housing starts are expected to increase about 10 percentrnand total home sales to rise nearly 8.0 percent in 2015. They also marked down theirrnprojected purchase and refinance originations. rnThey expect total mortgage originations to increase approximately 20rnpercent to $1.42 trillion, compared with a 24 percent gain in the priorrnforecast, with the refinance share remaining at 47 percent.</p<p

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment