Blog

FHA Issues Annual Report to Congress

CarolrnGalante, FHA’s new acting commissioner presented highlights of the agency’srnFY2011 Report to Congress in a press briefing on Tuesday, telling reportersrnthat FHA’s Mutual Mortgage Insurance Fund (MMI) will return to mandated levelsrnslightly ahead of schedule and that the agency is continuing to work its wayrnthrough its legacy loan losses. </p

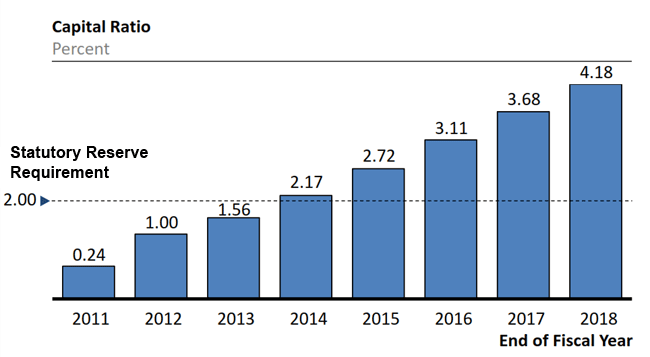

FHA’s capital reserve ratio measuresrnreserves in excess of those needed to cover projected losses over the next 30rnyears. The independent actuarial reviews of the MMI Fund estimaternFHA’s capital reserve ratio to be 0.24 percent of total insurance-in-force thisrnyear, falling from 0.50 percent in 2010. Congress has mandated a capital reserve ratiornof 2.0 percent. FHA’s total liquidrnassets (cash plus investments) grew by $800 million since last year, to $33.7rnbillion. That amount is $1.9 billion higher than at the end of FY 2009, and isrnalso $7.7 billion higher than was predicted last year by the independentrnactuaries. At the same time, the economic net worth of the Fund fell by $2.1rnbillion this year, from $4.7 billion to $2.6 billion, as FHA continued to buildrnloss reserves to prepare for greater claims in the coming years</p

A number of factors have negativelyrnimpacted the evaluation for the year, including:</p<ul class="unIndentedList"<liAnrnadditional 5 percent decline in home prices in the base-cast forecast;</li<liIncreasingrnnumbers of active loans with previous defaults.rn</li<liThernlarge number of loans caught in lengthy period of serious delinquency andrnforeclosure due to litigation and settlement discussions over servicingrnconcerns;</li<liAnrnactuarial assumption that the above concerns will lead to insurance claimsrnrather than another form of resolution.</li</ul

The actuaries find that FHA’s currentrnunderwriting and premium structure have created a sound basis for growingrncapital at a rapid rate once the economy and housing markets stabilize andrntheir base-case projections show capital ratios reaching the mandated 2 percentrnin 2014, earlier than was projected in last year’s report. This three-year recapitalization projectionrnmatches FHA experience in the 1991-94 period.</p

</p

</p

</p

</p

The book of business generated from Q2rn2009 is expected by the actuaries to be profitable, providing significantrnrevenues to offset losses from earlier business. Final losses on loans endorsed from 2000rnthrough the first quarter of 2009 are expected to exceed $26 billion with 2008rnalone costing close to $10 billion. rnClaim rates on 2006-2008 loans could go over 20 percent.</p

Though they were prohibited in 2009, thernongoing effect of so-called “seller-funded downpayment assistance loans” isrnstill significant. The net expected cost of those loans, as projected by thernindependent actuaries, grew by $1.8 billion over the past year to $14.1rnbillion.</p

Net income generated by businessrngenerated since Q2 2009 is $18 billion and early payment default rates are a negligiblern.35 percent compared to 2.23 percent in January 2008. Under the base-case forecast used by the actuaries,rnthe FY 2012 book will add an additional $9 billion in economic value to thernFund.</p

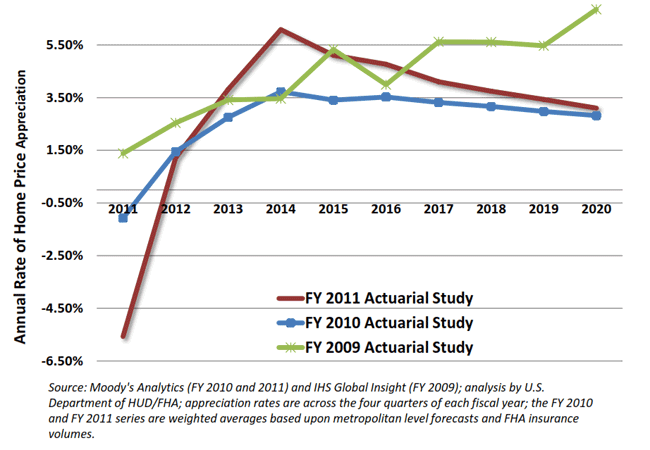

The base-case scenario from Moody’srnAnalytics indicates price declines this year of 5.6 percent and a smallrnincrease of 1.3 percent in 2012 followed by steady growth. Galante cautioned that there are remainingrnrisks including continuing significant declines in home prices which wouldrnrequire addition support for the current portfolio. The first support would come from the FY2012rnbook of business, estimated to be worth $9 billion. Actuarial estimates indicate that pricerndeclines in 2012 would have to rival those of 2011 before support beyond thisrnwould be needed. In that event, however,rnFHA would implement policy changes including additional premium increases. Only under the worst case would FHA look tornthe Treasury for support, but under current law it has permanent and indefiniternbudget authority to do so. </p

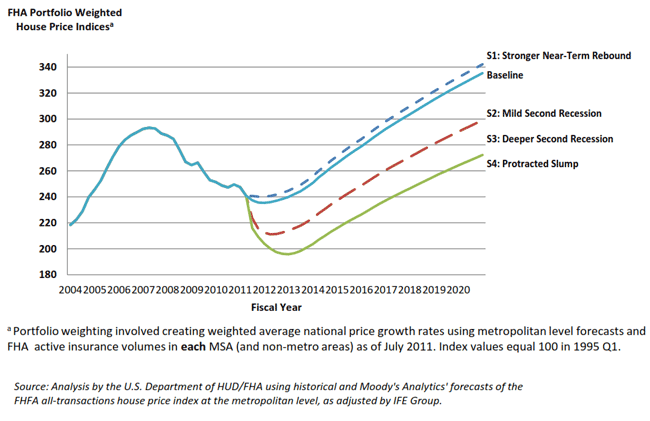

Galante said that the worst case homernprice scenarios are based on extreme declines in value occasioned by a secondrnrecession creating a 9 percent decline beyond the 5.6 percent decline in thernbase-case and there is no evidence this will happen. She said that the fund could withstand anrnadditional 4 percent decline in prices beyond the base case withoutrnexperiencing a negative capital situation.</p

</p

</p

FHA has taken steps to effectivelyrnmanage future risk:</p<ul class="unIndentedList"<liPremiumsrnhave been increased for single-family and HECM (reverse mortgage) programs andrnboth are at historic highs.</li<liChangesrnhave been made to the HECM program including development of the HECM Saver andrnnew guidance for lenders for treatment of tax and insurance defaults.</li<liArncomprehensive overhaul of single family loan review policies has resulted inrnchanges designed to strengthen lender monitoring.</li<liFHArnwill soon issue a final rule to strengthen the requirements for lendersrnparticipating in the Lender Insurance Program.</li<liFHArnis obtaining 21st century information technology systems andrncontinues to develop and implement a comprehensive and integrated riskrnmanagement system. </li</ul

During the past year FHA has insured its thirdrnhighest dollar volume ever, $236 billion including $218 billion in singlernfamily and $18 billion in HECM loans on a total of 1.27 million loans. FHA provided financing for 770,000rnhomebuyers, 75 percent of them first time buyers and accounted for 56 percentrnof all first-time buyers. The agencyrnalso provided refinancing for 440,000 homeowners and hit the 40 million markrnfor the total number of single family loans guaranteed by the agency.</p

During the year FHA cured 362,000 defaults and wasrnworking on 155,000 open cases to develop loan reinstatement plans. There had also been 26,000 short sales. The re-default rate on these loans in thernlowest in the last five years and is down 8 percent from last year.</p

Galante was asked at the press conference aboutrnthe impact of new, lower loan limits that went into effect on October 1. While it is too early to be definitive, shernsaid, there will probably be little impact as higher balance loans constituternonly 5 to 6 percent of FHA’s total portfolio. rnIf Congress should mandate a return to the higher levels for FHA but notrnfor Fannie Mae and Freddie Mac, a plan currently under discussion, Galante saidrnthe agency would be happy to implement it but, as it would be breaking newrnground, she would not estimate how much new business it might generate.</p

Another question involved the possibility ofrnreevaluating the fees for a Streamline refinancing to make it possible for morernpeople to refinance. Galante said thatrnFHA had not yet done an analysis to see how many people might benefit fromrnreducing or eliminating fees but that these fees were factored into actuarialrnprojections and to change them would change the trajectory of the actuarialrnprojections.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment