Blog

HAMP Running Out of Qualified Borrowers to Rescue

The Obama Administration has released April data for the HomernAffordable Mortgage Program (HAMP).

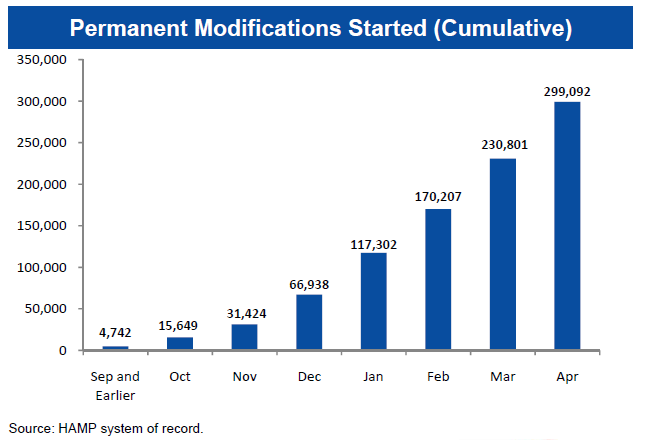

The number of homeowners who completed HAMP's mandatory 90 day trial period and were convertedrninto permanent load modification status rose 68,000 to 299,092 in April. This is a 13 percent increase over the number of permanentrnmodifications reported up until the end of March.

All of the borrowers who received permanent modificationsrnreceived a reduction in their loan interest rate; 53.4 also received anrnextension of the loan's term and 28.6 were given principal forbearance.

According to the report, lower monthly mortgage payments for borrowersin active trial and permanent modifications represent a cumulativepayment reduction of more than $3.1 billion to date. The median savingsfor borrowers in permanent modifications is $516.09, or 36% of themedian before-modification payment.

FHA Commissioner and HUD Assistant Secretary for HousingrnDavid Stevens said, “As the number of homeowners receiving permanentrnmodifications continues to increase, the Administration's comprehensiveeffortsrnare making an impact in the housing market's overall recovery. Todaymortgage rates remain at historic lows,rnaround five percent; foreclosure starts are down 27 percent from lastyear thisrntime; and home prices and the pace of home sales have stabilized inrecentrnmonths.”

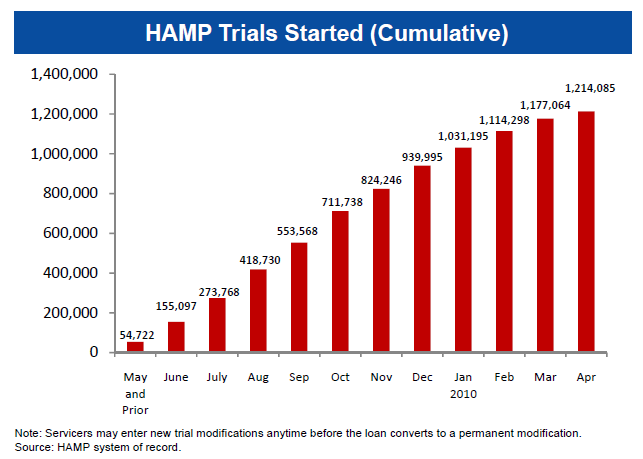

47,160 new borrowers had began trial loan modifications at the end of April. Of the 1,487,594 offers that were been extended, 1,214,085 borrowers have enrolled in the program.

In terms of the overall conversion rate, 20.1 percent of all offersextended have been converted to permanent loan modifications, muchimproved from last month's rate of 16.1 percent.

When measuringperformance against the number of HAMP trial offers that have actuallybeen accepted, 24.6 percent of homeowners who have completed the 3-monthrn period have been converted to a permanent modification. Again, much improvedfrom the 19.8 percent conversion rate reported in March.

The primary criticism of HAMP almost from the beginning hasrnbeen the low rate of loan modifications that were converted to permanentrn statusrnafter the mandatory 90 day trial program. rnWhile over 900,000 homeowners had entered the HAMP program by the end ofrn2009, fewer than 70,000 had been converted to permanent status. It wasto be expected that conversions would tricklernin initially, but many loans seemed stuck in trial status.

Since thefirst of the year, programrnadministrators have attempted to isolate the problems that were leadingto delaysrnand/or failures in conversion and have employed a number of measures toimprovernperformance.

“The number of homeowners receiving significant relief through a mortgage modification continues to rise,” said Chief of Treasury's Homeownership Preservation Office (HPO) Phyllis Caldwell. “Our focus now is on improving the homeowner experience and holding servicers accountable for their performance. Increased transparency through more robust reporting of servicer-specific data will contribute handily to those efforts.”

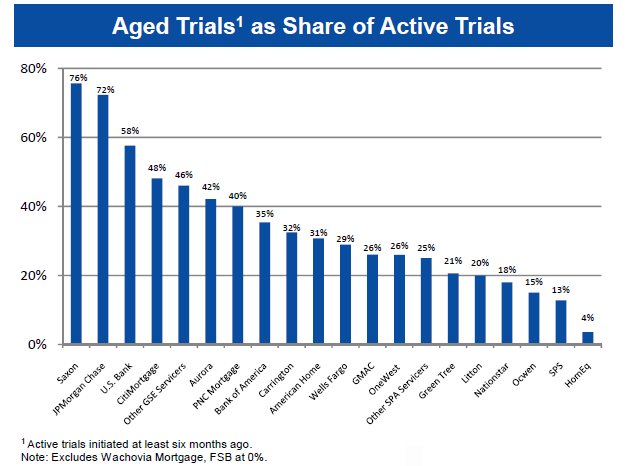

The April report unveils a new metric which gives servicer-specificrninformation on rates of borrower conversion from trial to permanentstatus. The Treasury Department said that the datarnshows that there is wide variation among servicers in these areas,furtherrndemonstrating the need for transparency regarding servicerperformance.” In fact, the data should make a couple ofrnservicers very uncomfortable.

Two servicers – Saxon and JPMorgan Chase – had stunninglyrnhigh numbers that had been in trial for six months or more, 76 percentand 78rnpercent respectively. These two werernalso among the servicers with the lowest conversion rates at 28 and 21percent.rn Saxon is among the smaller companiesrnhowever JPMorgan services the second largest pool of HAMP eligibleloans.

The Department alsorntold servicers of new reporting requirements that will go into effect inrn June. The new reporting will include information onrncompliance with program guidelines, program execution, and homeownerexperiencernincluding servicer handling of calls from homeowners, the time it takestornresolve programs reported by third parties such a housing counselors andrnattorneys, and the servicer's share of homeowner complaints to theHomeowner'srnHOPE Hotline. READ MORE

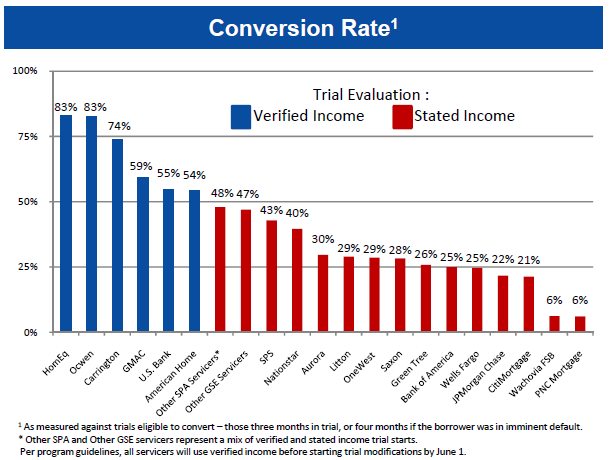

The importance of one change that will go into effect onrnJune 1 is demonstrated by the servicer-specific data on conversion ratesrn andrnthe numbers of aging trials. Initially,rnservicers made the decision whether to begin the trial modificationperiodrnbefore or after all required document were received and verified. Manyservicers used stated income in order tornget trials started and then collected income verification during thecourse of therntrial. The new data makes it clear thatrnthis is not working, and effective June 1 servicers must have borrowerrndocuments in-hand before offering borrowers a trial modification.

Without exception, those servicers with a conversion rate overrn50 percent have begun trials only after borrowers had supplied therequiredrndocuments. Without exception those that were relying on stated incomeandrnverification to company had conversion rates under 50 percent.

MND has discussed recent Administration initiatives to motivate servicers to play arn bigger role in helping families save their homes, but we wonder if servicers are totally to blame or if the Administration is starting to scramble as the HAMP program may be close to helping all who are capable of being helped.

Borrowers continue to report that the overwhelming reasonrnfor their financial difficulties is loss of income. 60.4 percent saythat was their primaryrnreason for needing a modification. 10.2rnpercent cited excessive obligations and 10.2 percent said it was theillness ofrnthe primary borrower. 77.1 percent ofrnborrowers were in default when they entered the program while 23.9percent werernat risk of default.

Combine those stats with the factthat 6.7rn million Americans have been unemployed for longer than 27 weeks andrn it's easy to see why HAMP is failing to convert more borrowers intopermanent loan modifications.

HAMP estimates that there are 3,275,249rndelinquent loans and 1,702,134 borrowers that are eligible for a HAMPmodification. With 1,487,597 trial offers already extended to the 1,702,134 pool of eligible borrowers and the number of Americans without a job for longer than 27 weeks continuing to rise, it appears HAMP may be running out of qualified borrowers.

The true test of HAMP'ssuccess will be whether or not permanent loan modifications are able toavoid re-default.

THIS SIGTARP REPORT calls attention to several factors limiting the effectiveness of HAMP.

HERE are some outspoken opinions on the subject.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment