Blog

Home Builders Waiting for Labor Market to Improve. Nervous About Foreclosures

From the National Association of Home Builders:

Builder confidence in the market for newly built, single-family homes declined one point to 15 in January on continuing concerns about the poor job market and large number of foreclosed homes for sale.

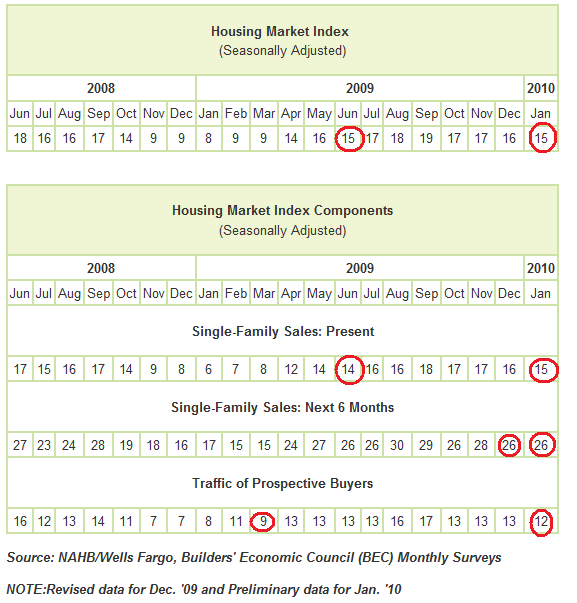

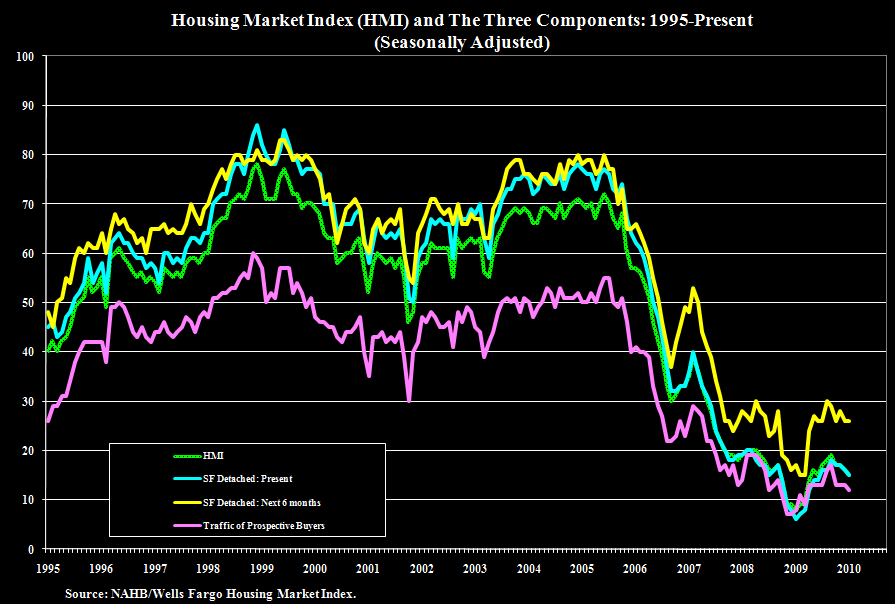

Derived from a monthly survey that NAHB has been conducting for morernthan 20 years, the NAHB/Wells Fargo Housing Market Index gauges builderrnperceptions of current single-family home sales and sales expectationsrnfor the next six months as “good,” “fair” or “poor.” The survey alsornasks builders to rate traffic of prospective buyers as “high to veryrnhigh,” “average” or “low to very low.” Scores for each component arernthen used to calculate a seasonally adjusted index where any numberrnover 50 indicates that more builders view sales conditions as good thanrnpoor.

The January HMI fell one point to 15, its lowest point since June ofrn2009.

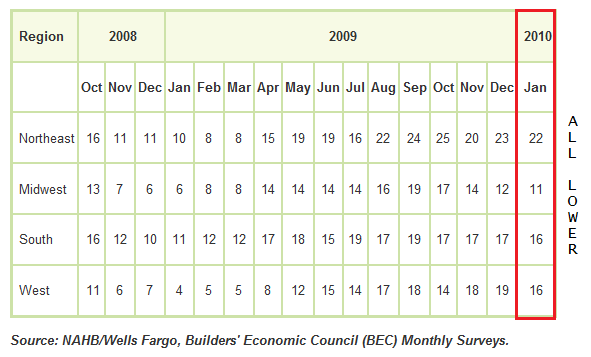

The HMI edged down by a single point in three regions, with the Northeast falling to 22, the Midwest down to 11 and the South declining to 16. The HMI fell three points in the West, to 16.

Two of its three component indexes registered one-point declines,rnwith the index gauging current sales conditions and the index gaugingrntraffic of prospective buyers falling to 15 and 12, respectively. Thernindex gauging sales expectations, in the next six months (YELLOW) held even, atrn26, but remains very low.

Here is a table of the data:

Here is a chart:

Here are some quotes from NAHB Chairman Joe Robson, a home builder from Tulsa, Oklahoma:

“At this point, home builders have done everything we possibly can to set the stage for a housing recovery – we’ve thinned our inventories, we’ve kept new construction to a minimum, and we’ve fought for and achieved a great new buying incentive with the extension and expansion of the home buyer tax credit,”

“We stand poised and ready to deliver new homes as soon as our customers are ready to take advantage of the tax credit and other historically good buying conditions in terms of interest rates, selection, and prices. Yet builders also realize that factors beyond our control – including consumer concerns about job security and competition from foreclosed homes on the market – are still impeding demand for new homes at this time.”

Here are a few more comments from NAHB Chief Economist David Crowe:

“Home buying conditions have rarely been as good as they are right now, but consumers are still waiting to see significant positive signs of improvement in employment and confidence, and this is slowing buyers’ return to the market,”

“Meanwhile, competition from foreclosed homes is also severely impacting new-home sales. That said, expected improvement in the job market this spring will help propel the housing recovery as we head into the prime home buying season.”

Plain and Simple: builders are ready to start working on new inventory, but are not likely to do so until the labor market improves. The NAHB is hopeful this will occur sometime this spring. MND is less optimistic but still waving our pom-poms.

READ MORE about MND's outlook

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment