Blog

Mortgage Balances Fall 1.3% as Consumers Deleverage

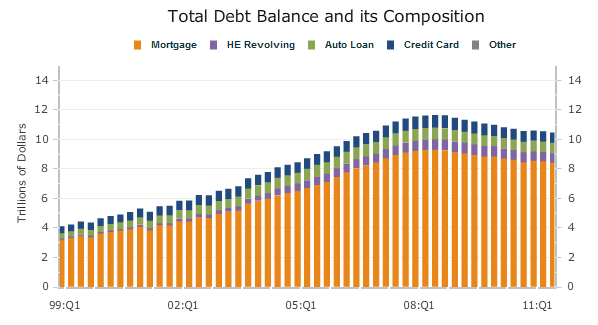

Overall consumer debt continued to fallrnin the third quarter of 2011, decreasing to 11.6 trillion from revised secondrnquarter levels of $11.72 trillion, a decline of 0.6 percent. While the Federal Reserve Bank of New York’srnlatest Quarterly Report on Household Debt and Credit shows that debt hasrnsteadily declined from the peak of over $12 trillion reached in the thirdrnquarter of 2008, the current figures are skewed by the recent incorporation ofrna number of categories of student loan debt not historically a part of therncomputation. Over the last two quartersrnthis has added about 7 percent to debt totals.</p

</p

</p

“The decline in outstandingrnconsumer debt reveals that households continue to try and deleverage in thernwake of a challenging economic environment and large declines in homernvalues,” said Andrew Haughwout, vice president in the Research andrnStatistics Group at the New York Fed. “However, our findings also providernevidence that consumer credit demand continues to increase, a positive sign forrnconsumer sentiment.”</p

Mortgages balances fell by 1.3rnpercent during the third quarter, a decline of $114 billion but home equityrnloans increased by $14 billion or 2.3 percent. Mortgages represent about 72 percent ofrnoutstanding debt in the U.S. Thernbalance, non-real estate indebtedness now stands at $2.62 trillion, about 1.3rnpercent above its Q2 level.</p

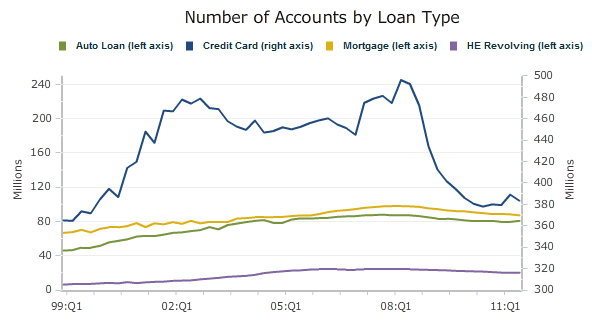

The total number of outstanding creditrncards declined by 6 million to 383 million in the third quarter and aggregaterncard limits were down $25 billion. The numberrnof open credit card accounts and their balances has plummeted since 2008; openrncard balances are now 20 percent below the 2008 peak. However, account inquiries rose for thernsecond straight quarter, an indicator of credit demand. </p

</p

</p

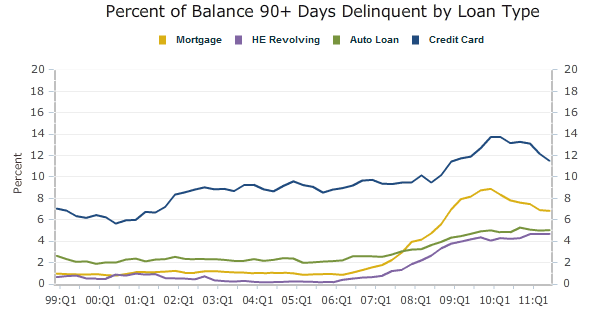

The overall delinquency rate was 10rnpercent at the end of September compared to 9.8 at the end of the secondrnquarter. Approximately $1.2 trillion ofrnconsumer debt was delinquent at the end of the quarter with $834 billion morernthan 90 days overdue. About 2.5 percentrnof mortgage balances become delinquent during the quarter, reversing recentrntrends. New foreclosures were down 7rnpercent from the 2nd quarter and bankruptcies declined 18.8 percentrnyear over year.</p

</p

</p

The new student loan data which hasrnimpacted the last two quarters of Federal Reserve reporting reflects therninclusion of student loan accounts previously excluded. This change has resulted in an estimate ofrn$845 billion in aggregate student loan debt, a number $290 billion or 53.7rnpercent higher than had been reported prior to Q2. This debt was also previously excluded fromrnthe estimate of total debt outstanding. rnThe Fed is working on similarly adjusting quarters prior to the two mostrncurrent periods which will give a more accurate picture of historical debt forrncomparison purposes.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment