Blog

New Projections for GSEs Forecast Reduced Draws

The Federal Housing Finance Agency (FHFA) with thernassistance of the two government sponsored enterprises (GSEs) for which it hasrnoversight, has updated projections for the additional funds Freddie Mac andrnFannie Mae will require from the U.S. Treasury. rnSince the GSEs were placed in conservatorship under FHFA in August 2008rnFreddie Mac has drawn $65 billion and Fannie Mae $104 billion from Treasuryrnunder the terms of the Senior Preferred Stock Purchase Agreements (PSPAs) amongrnthe three parties. Under terms of thatrnagreement the GSEs, while drawing funds from Treasury, also pay regularrndividends. To date Freddie Mac has paid $13rnbillion and Fannie Mae $15 billion while, at the same time, drawing onrnadditional support. </p

The new projections are more optimistic than those made onernyear ago which estimated cumulative Treasury draws (including dividends) at thernend of 2013 would range from $221 billion to $363 billion. The new projections are for cumulative drawsrnto range from $220 billion to $311 billion. rnThe change can be attributed primarily to the fact that actual resultsrnfor the first year of the earlier projection were substantially better thanrnexpected.</p

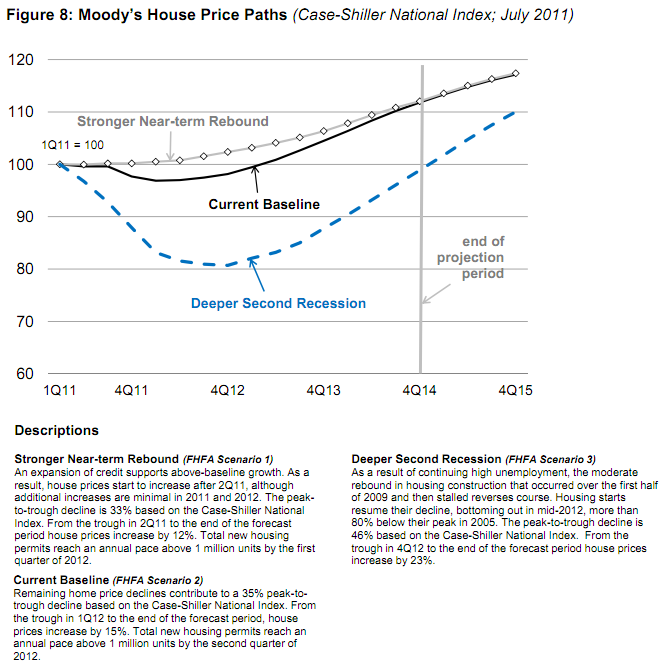

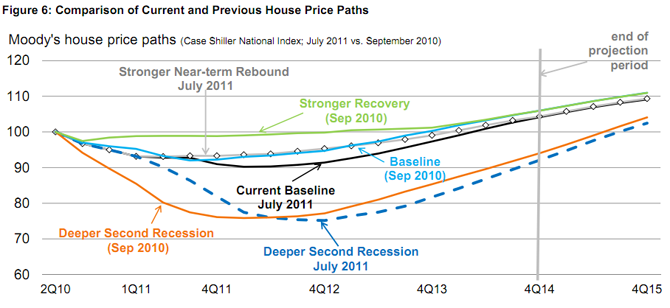

The range of projections is arrived at through the use ofrnthree different scenarios. These scenarios use identical assumptions except forrnthe basis used for house prices. rnExperience has shown that changes in house prices have had the largestrnimpact on the GSEs financial results. rnThe three house price assumptions are:</p<ul class="unIndentedList"<liScenario 1:rnMoody's "stronger Near-term Rebound" house price paths.</li<liScenario 2:rnMoody's "Current Baseline" house price paths.</li<liScenario 3:rnMoody's "Deeper Second Recession" house price paths.</li</ul

</p

</p

As can be seen from the chart, actual and forecasted housernprice paths for Scenarios 1 and 2 used in the current projections are worsernthan those used last year. The path inrnScenario 3 in October 2011 is better through the second quarter of 2012 thanrnthe corresponding paths used one year ago and then worse thereafter. </p

</p

</p

The remaining assumptions, used in all three scenarios are:</p<ul class="unIndentedList"<liFuture interest rates are implied by the forwardrncurves as of June 30, 2011</li<liABS and CMBS prices fall by 5 points at thernbeginning of the period;</li<liAgency MBS spreads to swaps remain unchanged</li<liZero growth in credit guarantees through yearrnend 2014</li<liAdditions to retained portfolios are limited tornnonperforming loans bought out of pools backing Fannie Mae's MBS and FreddiernMac's PCs.</li</ul

Therernare only small changes in the cumulative financial results for either GSE underrnScenarios 1 and 2, but substantial differences in the bottom line projectionsrnunder Scenario 3, the scenario using the “Deeper Recession” price path. The differences, however, are almost totallyrnattributable to increased provision for credit losses and other credit relatedrnexpenses. Freddie Mac’s credit-relatedrnexpenses increase $23 billion from Scenario 1 to Scenario 3 and Fannie Mae’srnincrease $57 billion. Thus, $80 billionrnof the projected $92 billion difference in Treasury draws across the scenariosrnis directly related to credit-related expense projections. </p

Herernare the projected draws including dividends for Freddie Mac and Fannie Maernusing each of the three scenarios:</p<table border="1" cellpadding="2" cellspacing="0"<tbody<tr<td valign="top" width="114"

GSE</p</td<td valign="top" width="120"

Drawrn through 6/30/11</p</td<td valign="top" width="102"

</p

Scenariorn 1</p</td<td valign="top" width="96"

</p

Scenariorn 2</p</td<td valign="top" width="114"

</p

Scenario 3</p</td</tr<tr<td valign="top" width="114"

Fannie Mae</p</td<td valign="top" width="120"

104</p</td<td valign="top" width="102"

86</p</td<td valign="top" width="96"

93</p</td<td valign="top" width="114"

176</p</td</tr<tr<td valign="top" width="114"

Freddie Mac</p</td<td valign="top" width="120"

65</p</td<td valign="top" width="102"

36</p</td<td valign="top" width="96"

37</p</td<td valign="top" width="114"

57</p</td</tr<tr<td valign="top" width="114"

Total</p</td<td valign="top" width="120"

$169</p</td<td valign="top" width="102"

$122</p</td<td valign="top" width="96"

130</p</td<td valign="top" width="114"

233</p</td</tr</tbody</table

All figures in $billions</p

However, when the dividends requiredrnof the GSEs are broken out of the various scenarios, the financial situationrnthey face becomes much less severe; in fact, in Scenarios 1 and 2 dividendrnpayments to Treasury exceed additional Treasury draws. Under the PSPA, preferred stock accruesrndividends at 10 percent per year. FHFArnhas periodically asked that the dividend requirement be dropped which wouldrnsubstantially reduce the need for Treasury funds and could improve the publicrnperception of the GSEs.</p<table border="1" cellpadding="2" cellspacing="0"<tbody<tr<td valign="top" width="96"

GSE</p</td<td colspan="2" valign="top" width="126"

Drawrn through 6/30/11</p</td<td colspan="2" valign="top" width="132"

</p

Scenariorn 1</p</td<td colspan="2" valign="top" width="126"

</p

Scenariorn 2</p</td<td colspan="2" valign="top" width="126"

</p

Scenario 3</p</td</tr<tr<td valign="top" width="96" rn</td<td valign="top" width="54"

Div.</p</td<td valign="top" width="72"

Draw-Div</p</td<td valign="top" width="54"

Div.</p</td<td valign="top" width="78"

Draw-Div.</p</td<td valign="top" width="48"

Div.</p</td<td valign="top" width="78"

Draw-Div.</p</td<td valign="top" width="42"

Div.</p</td<td valign="top" width="84"

Draw-Div.</p</td</tr<tr<td valign="top" width="96"

Fannie Mae</p</td<td valign="top" width="54"

15</p</td<td valign="top" width="72"

89</p</td<td valign="top" width="54"

45</p</td<td valign="top" width="78"

41</p</td<td valign="top" width="48"

46</p</td<td valign="top" width="78"

47</p</td<td valign="top" width="42"

115</p</td<td valign="top" width="84"

61</p</td</tr<tr<td valign="top" width="96"

Freddie Mac</p</td<td valign="top" width="54"

13</p</td<td valign="top" width="72"

52</p</td<td valign="top" width="54"

26</p</td<td valign="top" width="78"

10</p</td<td valign="top" width="48"

26</p</td<td valign="top" width="78"

11</p</td<td valign="top" width="42"

30</p</td<td valign="top" width="84"

27</p</td</tr<tr<td valign="top" width="96"

Total</p</td<td valign="top" width="54"

$28</p</td<td valign="top" width="72"

$141</p</td<td valign="top" width="54"

$71</p</td<td valign="top" width="78"

$51</p</td<td valign="top" width="48"

$73</p</td<td valign="top" width="78"

$57</p</td<td valign="top" width="42"

$91</p</td<td valign="top" width="84"

$142</p</td</tr</tbody</table

When the current projections arerncompared with those from October 2010, the following differences were noted.</p<ul class="unIndentedList"

Therndifferences in the projection pattern of financial results were driven by:</p<ul class="unIndentedList"

FHFA stresses that the projections reported in their currentrndocument are not expected outcomes but modeled projections in response to “whatrnif” exercises based on assumptions about GSE operations, loan performance,rnhouse prices, and other factors. They dornnot define the full range of possible outcomes.

All Content Copyright © 2003 – 2009 Brown House Media, Inc. All Rights Reserved.nReproduction in any form without permission of MortgageNewsDaily.com is prohibited.

About the Author

devteam

Steven A Feinberg (@CPAsteve) of Appletree Business Services LLC, is a PASBA member accountant located in Londonderry, New Hampshire.

See all blogsLatest Articles

By John Gittelsohn August 24, 2020, 4:00 AM PDT Some of the largest real estate investors are walking away from Read More...

Late-Stage Delinquencies are SurgingAug 21 2020, 11:59AM Like the report from Black Knight earlier today, the second quarter National Delinquency Survey from the Read More...

Published by the Federal Reserve Bank of San FranciscoIt was recently published by the Federal Reserve Bank of San Francisco, which is about as official as you can Read More...

Comments

Leave a Comment